The article on the Effective Interest Rate continues our series on Financial Mathematics in Excel. The effective interest rate is a useful metric for comparing the returns of different financial products. Its explanatory power is similar to the Internal Rate of Return (IRR), as it essentially expresses the return on investment.

Effective Interest Rate in Practice – Where is it Used?

For typical consumers, this metric is rarely encountered. This is especially true since the mandatory disclosure of the Annual Percentage Rate of Charge (APR) for all credit products was introduced. 1 This means that predatory lenders can no longer manipulate consumers by quoting interest rates with different compounding periods (daily, monthly, etc.) or varying interest payouts. They can, but they are always legally required to disclose the APR – a standardized percentage indicating the total annual cost to the consumer, including all fees.

Practically, you will mostly encounter the effective interest rate in capital markets (bonds) and in banking when accounting for interest-bearing products. In accounting, the accrual principle applies: banks and firms must allocate revenues/costs daily (even without actual cash flow). For complex interest products, they calculate daily amounts using this rate and the day count conventions method.

Effective Rate – Definition and Formula

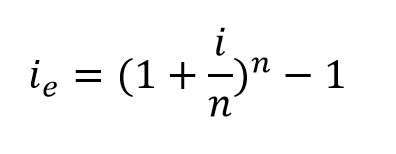

Textbooks in financial mathematics typically define it as:

Effective interest rate is the annual interest rate corresponding to a nominal rate that yields the same capital after one year, even if compounded n times per year. 2

Where:

- ie… effective interest rate

- n… number of compounding periods

- i… interest rate per compounding period (e.g., daily, weekly, monthly)

Admittedly, many people find this formula a bit abstract.

Effective Rate – Explanation with an Example

Imagine you are offered a bank product. Bank A offers a nominal interest rate of 5.3% p.d. (per day), while Bank B offers a similar product at 5.4% p.a. (per annum). For simplicity, assume the deposit period is one year and the invested amount is 1,000,000 USD.

At first glance, Bank B’s rate seems higher, but that doesn’t necessarily make it a better offer. Bank A compounds daily, which triggers the effect of compound interest – interest is added every day, and the next day interest is calculated on the updated balance. Bank B, in contrast, compounds annually.

We want to determine which investment is more profitable and how big the difference is in monetary terms.

(i) First, we calculate the effective interest rate, plugging the parameters of both banks (A and B) into the formula (see above):

After calculation, Bank A’s offer is more advantageous due to the compound interest effect (daily compounding), which accumulates enough over the year to surpass Bank B’s higher nominal annual rate.

Notice also that Bank B’s effective interest rate equals its nominal rate of 5.4% p.a., showing that the formula converts any nominal rate to an equivalent annual rate.

(ii) How much would choosing Bank B instead of Bank A cost if investing 1,000,000 USD? With both rates expressed as effective rates, the difference in returns can be calculated by multiplying the rate difference by the principal. For more precision, one can also use the compound interest formula for both options.

The difference for 1 million USD is approximately 425 USD. This would be the extra amount earned by choosing Bank A. As you can see, the difference is small from the perspective of an ordinary saver. These manipulations of compounding frequency are mainly relevant for investment and product specialists at large banks, where differences are measured in billions of USD and are much more significant. 🙂

>> Please download the excel and practise

Reference

- Investopedia, Annual Percentage Rate (APR): Definition, Calculation, and Comparison [on-line]. [cit. 2025-10-30]. WWW: https://www.investopedia.com/terms/a/apr.asp

- Corporate finance instaitute, Effective Annual Interest Rate [on-line]. [cit. 2025-10-30]. WWW: https://corporatefinanceinstitute.com/resources/commercial-lending/effective-annual-interest-rate-ear/